Oversubscribed Weekly #1

November 10, 2018This is the first edition of Oversubscribed Weekly: a weekly newsletter providing insights on seed fundraising from both founders and investors. Whether you’re about to fundraise or think you may in the future, reading this newsletter each week will make fundraising less intimidating and increase your fluency in the nuances of fundraising.

Before we jump into the first newsletter (which includes curated tweets and commentary about seed fundraising strategy, plus Q&A with a VC and founder about their experiences investing/fundraising), we have an exciting announcement.The second edition of our book, Oversubscribed, is now available on Amazon Kindle. The second edition includes even more examples and stories from anonymous VCs about the fundraising process. For the next 48 hours, it’s only $0.99, but after that, it’ll be back up to $9.99.

Buying the Kindle book helps us boost our Amazon rankings and get Oversubscribed in front of even more people.If you buy it and leave a review, send us a screenshot of your review and we’ll send you a seed round deck from a founder who recently raised $2M.

Tweets worth reading

Andrew Chen is a Partner at Andreessen Horowitz, and writes really valuable content about early stage growth for startups. In this thread, he dives deep into the metrics investors look at with early stage startups. Here’s a direct link to the (long) article.

Ok. This is written by Mike. As a founder, Mike sometimes did this, telling investors, “we’ve been invited by YC to apply and feel good about our chances.” While this can generate interest in the short term, ultimately it can (and usually will) backfire. First of all, accelerators invite a lot of startups to apply (even personally), but an invitation is far from a guarantee of getting in. If you don’t get in, and an investor asked how the application process is going, you’ll need to tell them that you didn’t get in, which will temper their excitement. If you do get in, fundraising will be much easier regardless of what you’ve told investors. Therefore, it’s rarely worth it to communicate accelerator interest to potential investors.

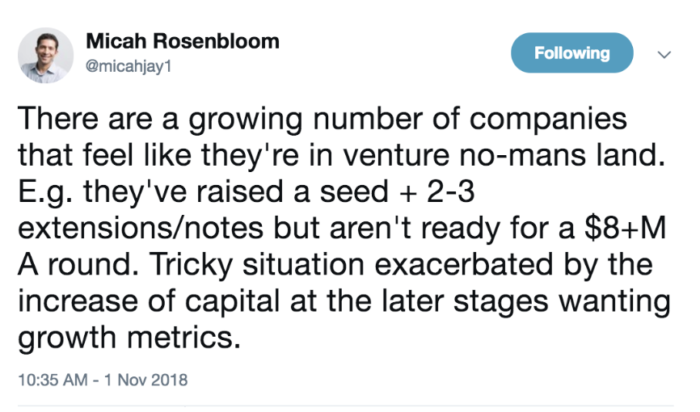

Micah Rosenbloom is a partner at Founder Collective. Since he’s a former founder himself, you can trust that he knows what it’s like to be on the other side of the table. That said, he’s clearly been in VC long enough to succumb to a humblebrag here and there. His insights are great, and here he warns about getting caught in-between Seed and Series A rounds.

When thinking about raising a seed round, it can be valuable to do your research and talk to Series A investors about what metrics they want to see in order to invest. That will help you set milestones and determine how much you need to raise to actually hit those milestones. (Also, Series A investors are incentivized to help you raise your seed round through introductions – they know that if they help you now, you’ll reach out to them if you do hit those milestones.)

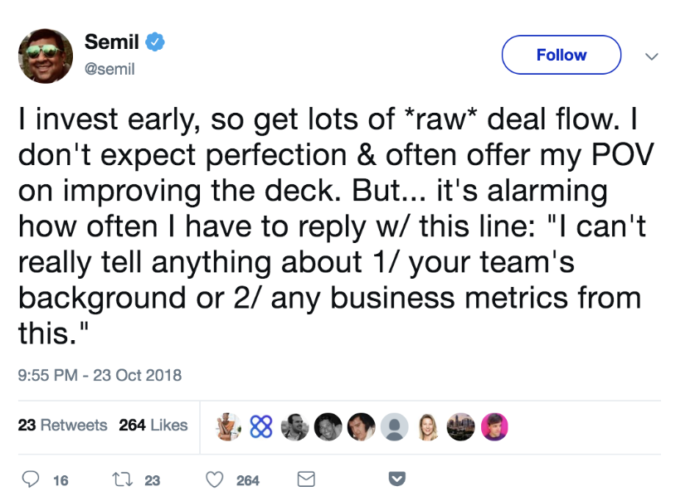

Semil Shah is a seed investor (he operates as a solo partner), and has great insights about fundraising/seed investing. This is a good reminder of what’s most important at the earliest seed stage. Make sure investors know why your team is special. Also, showing business metrics isn’t just about demonstrating traction – it’s about demonstrating that you understand the drivers of your business. This is also true about financial models. Perfect projections aren’t expected, but someone viewing your financial model should feel like you truly understand the math of your business.

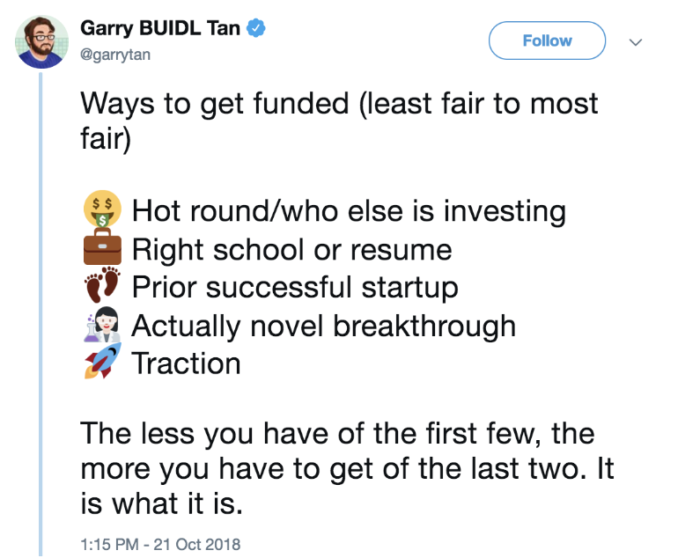

Garry Tan is a partner at Initialized Capital (with Alexis Ohanion, Serena Williams’ husband who I believe once created some website people like or something). There are exceptions these rules, but unfortunately he’s generally correct here. This is why it’s important to run a tight fundraising process than generates FOMO with investors – FOMO is far and away the biggest reason VCs and angels invest.

Q&A with an anonymous VC

Note: these Q&A’s are sometimes anonymous because that allows us to share the unvarnished truth.

Q: Have you ever been on the cusp of investing in one startup, but another startup came out of nowhere to beat them out?

A: “I’d been talking to a founder who pitched me 4 months ago. I gave him a verbal commitment that I wanted to invest 6 weeks ago, but the round has yet to come together. The founder has asked me some questions about terms before going to other investors, but he doesn’t seem to have a huge sense of urgency and it’s not clear who’s court the ball is in. I’ve been pretty busy with some other aspects of running the fund and haven’t been able to move things along for him.

Meanwhile, I was introduced to a second founder a month or so ago who was clearly a special founder. While the first founder has been a bit wishy washy in his approach, I was 100% confident that this second founder would raise his round with or without us investing. That makes me feel excited – he won’t need any handholding, and it’s clear that he’ll be well-equipped to raise subsequent rounds of funding.

Unfortunately, it feels like time has killed the deal with the first founder. From the time that I verbally committed and proposed a valuation, it took him 2 weeks to get back to me on my proposed terms. By that time, I had already met the second founder, who not only impressed me but made me feel like I was about to miss out on something that could be really big. While I originally had conviction on the first founder and startup, the sense of urgency and conviction that the second founder instilled made me lose conviction in the first founder.

I was able to make a commitment and wire my investment to the second founder within 10 days of our first call.”

Q&A with a founder

Q: What’s a fundraising tactic that worked for you, which you think more founders should think about?

A: “For individuals fortunate enough to graduate from college, you are part of that alumni network forever, though most people don’t leverage this resource effectively—or even at all. Upon graduation, I stayed on campus and continued to work for my alma mater, and I got to see just how eager alumni were to give back to the university, students, and other alumni. Most universities will have alumni networks with thousands of people—all with different skills, resources, and experiences. This is a deep well of easy to access knowledge, support, and even investment.

When I left to start working for a startup, I reached out to a number of alumni in the business world to ask for advice and mentorship as I embarked on my startup journey. I scoured the alumni database for people who had relevant experience and expertise, or people who just had a cool trajectory or story, like a biology major who now runs a massive tech company. I’d find their email on the alumni database (or ask the university resource center for their contact info if I couldn’t get it myself), send out cold emails with subject lines like “Greetings from an alumnus!”, ask to meet with them when I traveled through their city, or to hop on a call. Simply being curious and interested in how they got to where they are led to some amazing conversations, some great friendships, and even the first investment in the company I eventually founded.

Over the course of that first year working at a startup, I sent a lot of cold emails to alumni. I tracked my numbers too: I had a 75% response rate to my cold emails to alumni.

The door is already open, you just have to walk through it.”

—Dan Bloom, Slope

Enjoy this? Get Oversubscribed in your inbox every Thursday.